When I look at our top two performing equity managers this year I see: (i) a global manager with a focus on high quality, defensive names and (ii) a UK manager with a focus on unloved and cyclical companies. These feel like polar opposites to me: cheap, unloved Brexit Britain vs the best quality businesses the world has to offer (which, unsurprisingly, do not trade that cheaply). How are both doing well at the same time?

Part of the answer is, of course, the skill of the manager themselves. It is also not surprising to me that higher quality companies (which have, for example, less debt on their balance sheet) would do well when fears of a recession are on the rise. But what is the story behind the UK?

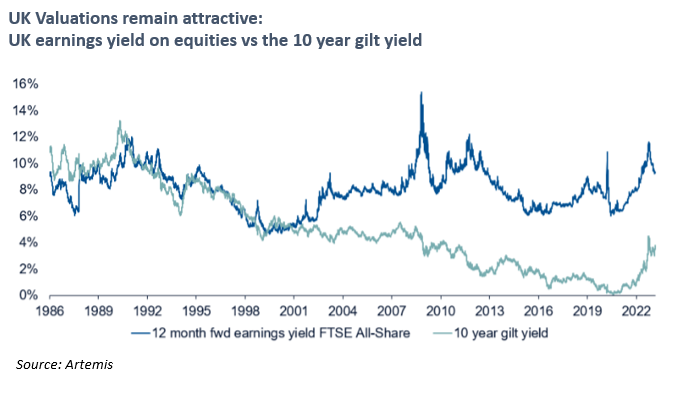

Here I would start with the fact that – unsurprisingly after everything we’ve been through these last few years – UK equities look cheap. And they still look cheap even after you allow for the fact that interest rates have gone up a lot in the last 12 months. The earnings yield you get on the UK equity market (so the profits companies make divided by the price you pay) is 10.0% currently. This is 6.3% more than the current 3.7% 10 year gilt yield and compares very well to longer term history (as the chart below shows). By comparison, the US has a 5.5% earnings yield today which is only just higher than the current 5.25% US base interest rate.

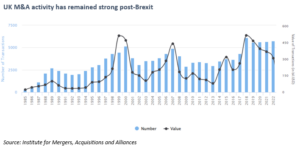

Low valuations and (especially for US investors) a cheap pound have meant that UK companies are seeing a pick up in mergers and acquisitions (M&A). Recently we have seen proposals, speculation or formal approaches on The Hut Group, Network, Wood group, Numis, Industrials Reit, Simcorp and Software AG to name but a few. This is a total $24.8bn of UK market cap potentially being taken private. The UK has become a favoured destination for global private equity investors. This, of course, helps put a floor on prices and – for the targets being acquired – gives an exit at a healthy premium to the old trading value.

Finally, UK companies got very little help from the UK government to help shield the pain of rising energy costs. Well, the good news is that the worst of this energy shock looks to be over. Despite recent cuts in production from OPEC, oil in the US is back below $70 a barrel. Even in the UK, oil is back in line with its average 20-year (inflation-adjusted) price range. And, as we show below, UK gas prices continue to fall.

Cheap valuations and an improving macro backdrop are often a recipe for good returns. The UK will, of course, struggle if and when the much talked about recession does eventually show up. But, even if it does, the longer-term opportunity looks pretty attractive from here.

For those that don’t know, I head the investment team at IPS Capital. Each week I highlight a few things that have come across my desk that I think are interesting and investment related. We always welcome dialogue so if you have any questions we’ll be happy to answer them.

Chris Brown

CIO

IPS Capital

cbrown@ips.meandhimdesign.co.uk

The value of investments may fall as well as rise and you may not get back all capital invested. Past Performance is not a guide to future performance and should not be relied upon. Nothing in this market commentary should be read as or constitutes investment advice.